Analysis of the model for determining the economic value of mined forest areas: A case study FE Vrbanja Kotor Varoš

DOI:

https://doi.org/10.7251/GSF2030008CKeywords:

economic value of forests,, economic value of forests, forest areas evaluation models, mined forest areasAbstract

The paper presents the results of research related to the application and improvement of the Model for determining economic value of mined forest areas, with specific application to the forest-economic area managed by Forest Estate (FE) Vrbanja Kotor Varos. It primarily points to the economic aspect of the problem of mined forest areas and, as a result of the research, the Model used to determine economic value of mined forest areas, developed by the author Nemanja Anikić, MA (2020), was analyzed. This Model includes performing six consecutive steps. The first step is a survey, which was used to gather the opinions and views of certain stakeholders. Two groups of participants, local population and employees of FE Vrbanja (a total of 30 respondents), were interviewed using questionnaires. The obtained results would be improved by increasing the number of respondents, increasing the number of open questions and, in certain situations, by applying the method of non-randomized sampling for the groups such as professionals, where the subjective judgment would be based on the experience and previous work of respondents with the subject issues.

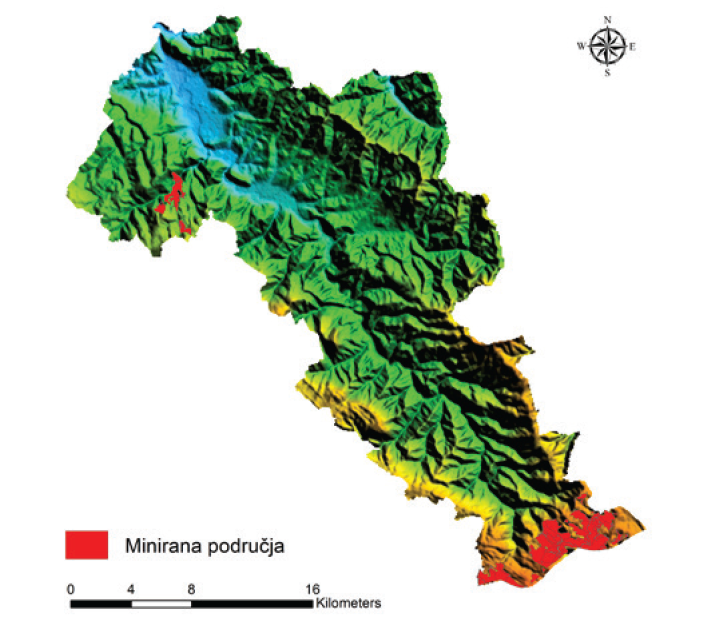

The results related to the analysis and graphical representation of areas under mines using geographic information systems (GIS), i.e. related to the second step, show that improvement is needed in terms of the use of specialized software packages, such as AutoCad Map. If there is a possibility, it would be desirable to use more modern versions of GIS programs since they provide greater possibilities. The limitation is their price.

The third step includes the methodology for estimating annual allowable cut, on the basis of which Anikić (2020) determined the state for one management period (10 years) with a volume of 90,620 m³, of which the largest part (85,885 m³) refers to high forests with natural regeneration. The improvement of the Model in this step is a potential collection of taxation data without physical contact in forests under mines using drones with high-resolution cameras, satellite images and using laser scanning (Lidar).

The fourth step is a methodology for determining the assortment structure, within which the scope and structure of wood assortments production by tree types for the next forest management period was determined using assortment tables. It was stated that the Model can be improved by creating new assortment tables.

Within the fifth step of the research, the total value of wood assortments on the truck route (income), which amounts BAM 6,280,744, was determined, while the costs of use (expenses) amount to BAM 2,666,040. The difference between income and expenses is profit before tax, and it amounts BAM 3,614,704, which confirms the Model justification. A significant improvement of the model would also refer to the valorization of the total values of mined forest areas which would, in addition to economic values, also include general useful functions of forests. Improvement can also be made through introducing new ways of analyzing business performance, i. e. classifying profit categories into several elements, in terms of profit before interest, taxes and depreciation (EBITDA) or profit before interest and taxes (EBIT), as well as calculations for partial economic indicators in terms of determining productivity, cost-effectiveness and profitability, depending on the available input data and/or projected trends. In theoretical terms, it is possible to consider a scenario which includes the costs of demining the terrain.

Sensitivity analysis is the last (sixth) step to be implemented. The improvement refers to the application of sensitivity analysis to other variables, as well as to the application of another approach to sensitivity analysis based on determining the percentage decrease (for example, volume) or increase (for example, utilization costs) of individual (critical) parameters so that the observed result (for example, profit) would at least be equal to zero (profitability threshold).

Downloads

Published

Issue

Section

License

Copyright (c) 2020 Dragan Čomić, Nemanja Anikić

This work is licensed under a Creative Commons Attribution 4.0 International License.